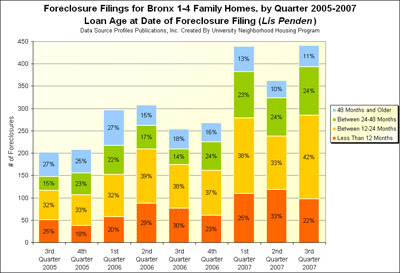

UNHP's recent analysis of foreclosure data for Bronx 1-4 family homes shows that the majority of loans going into foreclosure are less than two years old. For the first three quarters of 2007, 63%, 66%, and 64% of all loans going into default (having a lis penden filed) were made in the previous 24 months, respectively.

This data shows the extent of poor underwriting by lenders in 2005 and 2006, where clearly many loans were made in the Bronx without regards to the borrower's ability to repay. A good chunk of these loans could probably be considered predatory for this very reason, while others may just be bad loans. Based on research by a number of national groups, it's likely that many of these borrower's (often Black and Latino) qualified for better loans but were steered into mortgage products that maximized profits for brokers and loan officers.

It also is important to consider when thinking about solutions to the problem. Many proposals (including this one from the FDIC) call for freezing the introductory interest rates on so-called 2/28 and 3/27 mortgages, where a lower interest rate resets after the first two or three years to a higher rate for the remaining years on the 30 year mortgage. While this is not a bad idea and will help a percentage of homeowners, it will do no good for many Bronx borrowers.

Click here for a larger version of this chart, and more housing updates from UNHP.

You make alot of broad accusations regarding poor lender practices. Steering, targeting minorities, unfair pricing.

ReplyDeleteWhat I think is most amusing about your conclusion that because most (~66%) of foreclosures come from the past 2 years, that its indicative of poor (and illegal per your assessment) underwriting - however you fail to even mention that 67% of ALL ACTIVE loans in the Bronx area also were originated in the past 2 years.

I am not saying there isn't a foreclosure problem - there is. I am not saying that lenders are completely innocent - they are not. However, the bold statements in your blog here are very misleading, and only telling the part of the story that supports your claims - and by no means is a biased view on the current state of foreclosures.

Both Borrowers and Lenders share culpability here - and if you really want to do some research - you will see that the makeup of the loans in foreclosure has heavy concentrations of investment properties from people trying to make a quick buck - and just choosing to walk away when they were unable to make that quick buck...

I could go on - but whats the point?

Dear anonymous,

ReplyDeleteI'm not sure I share your amusement. The average age of loans going into foreclosure has been steadily decreasing (http://www.nytimes.com/2007/10/29/nyregion/29foreclose.html?ref=business), and I think represents a serious problem. If a loan is going into default in the first two years, unless the borrower has experienced a major catastrophe (e.g., loss of job, hospital/health bills, divorce), the lender was not doing their job to ensure the borrower would have the ability to repay the loan -- and that is the root of the problem here. Read this article if you are not convinced that loan officers were incentivized to steer borrowers into higher cost loans: http://www.nytimes.com/2007/08/26/business/yourmoney/26country.html?_r=1&ei=5087%0A&em=&en=a1ae7e7968332e0f&ex=1188360000&pagewanted=all&oref=slogin

Where is your data coming from on the active loans, may I ask? If I'm failing to cite such an important statistic, you could at least give me your source.

Finally, our research focuses on the Bronx. Do you have any statistics on how many of the foreclosures in the Bronx are against investors? We haven't run into any of them, but also haven't had the time to run all the numbers on this. Maybe you can share your source on this piece of information as well.

you can check either loan performance or McDash analytics for the statistic. for the information on active loans for the industry.

ReplyDeleteI am NOT saying its not a problem, and I am not saying there was no "steering" of customers towards higher cost loans (this is a broker caused problem, though, NOT a lender caused problem - lenders are NOT equal to brokers)

What I am saying is that simply by itself, a reducion in the average age of loans in foreclosure is not indicative of poor underwriting (do I think lenders pushed the envelope too far? - yes I do).

There HAS to be culpability on both sides though - lenders should not be putting people in homes they cannot afford, but borrowers also need to be responsible for understanding what they are getting into.

Are age of foreclosures decreasing - I have not studied it, but I will assume its true based on your sources - ONE reason this is happening is because the average age of loans has decreased because of the massive refinance boom we had between 2002 and mid year 2005. It was the best of times, home values were growing at double digit rates, interest rates were extremely low and lenders were competing with each other to see who could grab as much market share as possible.

There is a problem in our country however, with many media sources (yes, I lable your story above as such) not giving the whole truth. You cannot say "age loans in foreclosures is <2 years now - obviously there was lender malfeasance. If NOTHING had changed with HPI (house prices), interest rates, etc - which coupled with the egregious lending practics is causing the problem - you would STILL have a reduction in the average age of foreclosures simple because SO MUCH of our active loan population is so young now.

The main point of the original post was that freezing the interest rates of 2/28 and 3/37 mortgages would not have quite the impact that many think, since so many loans are going into foreclosure before they reset.

ReplyDeleteI understand your point that there are more loans that are younger now because of all the refinancing, but that doesn't change the fact that so many of these loans are in default so soon. The problem, of course, is not only that there are a higher percent of young loans in default, but that there are so many more of them now.

Who you want to blame for these poorly underwritten loans is up to you, but you can't deny that the vast majority of these loans that are going into foreclosure so quickly were not made with great concern for the borrower's ability to repay.

This data shows the extent of poor underwriting by lenders in 2005 and 2006, where clearly many loans were made in the Bronx without regards to the borrower's ability to repay.

ReplyDeleteBoth Borrowers and Lenders share culpability here - and if you really want to do some research - you will see that the makeup of the loans in foreclosure has heavy concentrations of investment properties from people trying to make a quick buck - and just choosing to walk away when they were unable to make that quick buck...